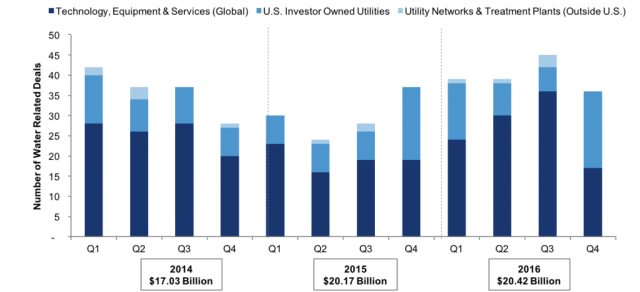

Mergers & acquisitions (M&A) in the global water sector exceeded $20 billion in 2016, pushing the three-year total valuation of announced deals to more than $57 billion, according to a new report, Water Mergers & Acquisitions: Key Trends in a Changing Global Landscape. Bluefield Research’s in-depth analysis of 447 transactions since 2014 highlights key shifts in the competitive landscape as companies position to address increasing municipal and industrial needs for water & wastewater infrastructure solutions.

“The types of deals and breadth of companies building out positions by acquisition are positive signals for water sector growth,” according to Reese Tisdale, President of Bluefield Research. “Broader market forces, including poor water quality in Flint, growing population demands, and increasing risks to industrial company bottom-lines, whether they be in energy, power, brewing, or mining, underpin deal flow among companies angling to be at the forefront of this change.”

Since 2014, 63% of the 447 deals tracked quarterly by Bluefield have been focused on technology, equipment & service companies (e.g. membranes, pipes, pumps, meters, EPC services). The remaining 37% feature utility network & distribution assets, including 113 investor-owned utility acquisitions in the U.S. and transfers of equity stakes in water treatment systems (e.g. desalination plants).

Over the last three years, the lion’s share of activity has been executed by strategic buyers moving to expand their positions across the water industry. At the top of this list is Suez’s $3.4 billion acquisition of GE Water, the largest pure-play water deal to date. This blockbuster deal, which drew a reported 72 interested parties, highlights a widespread focus on North America and the opportunities for growth in supporting the industrial sector.

“We are also seeing heavy deal flow among engineering and construction firms, which play a pivotal role in water infrastructure projects. These companies are often diversified across multiple sectors (e.g. energy, power, water), making Stantec’s 2016 acquisition of MWH Global unique. Because of MWH’s water sector focus, it thrust Canada-based Stantec into a global leadership role for water and wastewater services, overnight.” says Tisdale.

Bluefield’s analysis of deals across the industry value chain has uncovered several key trends that signal far-reaching impacts on the competitive landscape going forward:

- S. remains epicenter of deal flow. Of the 447 deals analyzed, 265 targeted companies are headquartered in the U.S. The $1 trillion infrastructure investment proclamations by the Trump administration, public concerns about water quality, and municipalities need to do more with less financially has bolstered investment sentiment towards technologies focused on efficiency and private participation.

- Advanced technology solutions usher new wave of growth opportunities. Whether it be for reclaimed wastewater for municipal and industrial reuse in the U.S., micro-pollutant treatment in Europe, or mining sector demand for alternative water supplies in Chile, water treatment & management solutions are becoming more sophisticated and economically attractive. As a result, consolidation of advanced technology suppliers will gain momentum, globally, as strategic buyers look to expand their portfolios through acquisition.

- Consolidating EPC sector impacting water. Over the past 36 months, leading engineering design firms, Stantec, AECOM, Arcadis, TetraTech, AMEC Foster Wheeler and Jacobs- have participated in more than US$11.7 billion of deal flow to recast their footprints and changed the competitive landscape among leading service providers.

- Japanese, emerging Chinese players navigating globe. A growing roster of critical infrastructure investors, such as Mitsubishi Corporation, Mitsui & Co., Beijing Water, and China Everbright, have secured beachheads in global hotspots, including Brazil, the U.K., Australia, and the Middle East. This activity could have longer-term impacts on competition for technology and utility ownership going forward.

“The one thing about water is that there is no one path for investment, and our ongoing analysis of the data reflects this.” says Mr. Tisdale.

About Bluefield Research

Bluefield Research provides data, analysis and insights on global water markets. Executives rely on our water experts to validate their assumptions, address critical questions, and strengthen strategic planning processes. Bluefield helps key decision-makers at municipal utilities, engineering, procurement, & construction firms, technology and equipment suppliers, and investment firms advance their water strategies. Learn more at www.bluefieldresearch.com.

About the Report

Water Mergers & Acquisitions: Key Trends in a Changing Global Landscape, provides an in-depth analysis of emerging trends in deal flow for advanced treatment technologies, EPC services, data & analytic solutions, and private ownership of networks & distribution, globally.

Comments